March 4, 2022

SALT Cap Workaround

Many of us have felt the pain of the 2018 Trump tax reform SALT cap (state and local tax). Prior to 2018, if you itemized your deductions, you were able to deduct the total of your state income tax, real estate property tax and personal property taxes paid. Since the reform passed, the maximum deduction allowed for that section is $10,000. If you’re a high earner, live in a high property tax state, or both, you’ve likely lost a large amount of annual tax deduction.

Congress has been using this deduction as a bargaining chip in their negotiations of potential tax law changes. President Biden wants to raise taxes on the highest earners but has offered to eliminate or increase the SALT cap to soften the blow. To date, Congress has not been able to agree to any changes, so as it stands, the $10,000 deduction limitation is still in place.

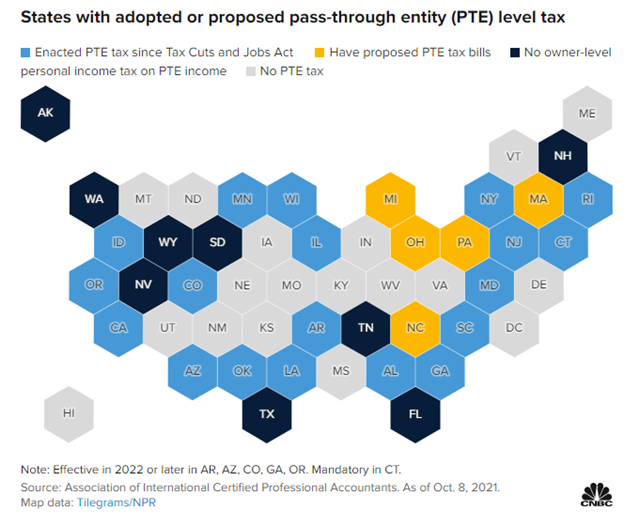

In the meantime, nearly 20 states (see graphic below for your state’s position) are offering workarounds for the write-off limit for certain businesses, and others have pending legislation. Although the IRS and U.S. Department of the Treasury have blocked some individual strategies to bypass the cap, some states have other methods for pass-through businesses, such as partnerships, S-corporations, and some LLCs.

In states that have PTET legislation, a pass-through entity elects to pay state-level taxes at the entity level, rather than passing on the full tax liability to individual owners, with state tax credit to individual owners for state taxes paid by the entity. The entity, which is not subject to the SALT cap, may claim a federal Section 164 business expense deduction, and shareholders may claim deductions for up to $10,000 for other state taxes paid on their individual returns, such as residential property taxes or state income taxes on other sources of income.

Whether you should utilize the workaround is unique to your personal tax situation and should be reviewed with your Crown advisor and CPA. If you own a pass through business in one of the blue states below, let’s start those conversations with your CPA so we can put you in the best tax position possible for 2022.

Nick Kolbenschlag – Chief Executive Officer & Co-Founder