January 10, 2024

2023 Recap and 2024 Preview

2023 Recap: From Gloom to Boom

It was a year of unexpected resilience for the U.S. economy and stock market.

Entering 2023, the stock market was shrouded in the anxieties of 2022. The previous year had witnessed a bruising bear market fueled by soaring inflation, rising interest rates, and the war in Ukraine. Wall Street braced for further turmoil last January, with a possible recession arriving in 2023. Instead, the economy defied those expectations and solidified a new bull market that charged forward in a remarkable comeback. The economists were caught offsides.

Crown clients benefited from the market upswing in 2023. Our goals-based and growth investing strategies delivered handsome returns.

Major indices surged with the S&P 500 climbing 24.2% and the Nasdaq up 43.4%. The Russell 2000 returned a solid 16.9% after a two-month rally that began on October 27th, off the lows for the year. U.S. bonds rallied sharply the final two months as well. The Bloomberg Barclays U.S. Aggregate Index finished up 5.3%.

That’s not how it was supposed to go. The consensus view of Wall Street strategists at the beginning of 2023 had it all wrong. To name a few, Morgan Stanley predicted the S&P 500 would tumble, Goldman Sachs pumped up Chinese stocks (-11% return), and Merrill proclaimed treasuries yields would sink. The opposite of consensus proved true, and many investors missed out on large swaths of the year’s gains.

Economists didn’t fare much better than stock strategists. First Trust’s highly respected, and often accurate, economist Brian Wesbury called for a recession in Q3. The result? GDP grew at a breakneck 5.2% for the quarter.

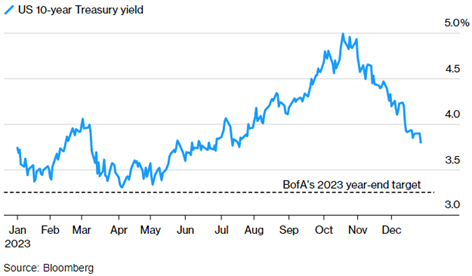

Their forecasts were not unfounded as interest rates took investors for a ride. The global benchmark 10-year U.S. Treasury yield started the year at 3.88%, climbing up to a high of 5.02% in October, then plummeted to end the year at 3.88%. A true rollercoaster, ending right back at the start.

Negative catalysts also emerged in March as the Silicon Valley Bank failed and the Treasury came to the rescue. The debt-ceiling debacle in Washington continued, mortgage rates rose well above 7%, and U.S. sovereign credit ratings were downgraded again.

War in Ukraine continued, and long latent hostility in the Middle East between Hamas and Israel erupted.

Stock market tailwinds nevertheless prevailed. The key drivers of market growth were cooling inflation, anticipated Fed policy change, and optimism surrounding artificial intelligence.

The Fed finally started reigning in their aggressive interest rate hikes by midyear as inflation abated. This shift in monetary policy alleviated concerns about economic slowdown. Inflation continued to retreat faster than anticipated, down to 3.1% in November.

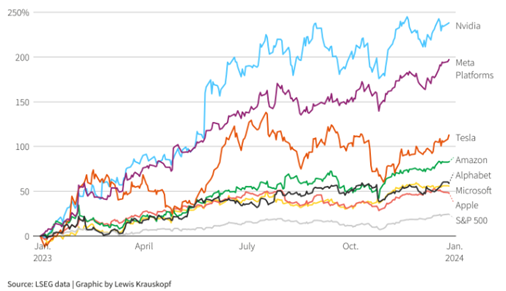

Advancements in artificial intelligence (AI) came strongly to the fore in 2023. Microsoft and other tech giants benefited. Dubbed the “Magnificent Seven,” these companies became market darlings and were the driving force behind the S&P 500 and Nasdaq’s gains.

The “Magnificent Seven”

Media outlets will have you believe all their success stemmed from recent AI-related developments and optimism about the technology’s potential. We believe America’s tech giants went through a healthy process of becoming mature companies by focusing on core businesses and significant cost-cutting after their 2022 market drubbing. Their formulae for innovation, growth, and massive profits remains intact as competition in AI ramps up around the globe.

From January anxieties to the final December flourish, the story of the S&P 500 last year offers a testament to the dynamic nature of the market and the ability of unforeseen factors to reshape its trajectory.

2024 Outlook

As we turn the page on 2023, uncertainties around geopolitics, strength of the consumer, and slowing economic growth indicators remain. We believe the resilience shown in 2023 gives plenty of reason for optimism.

Last year’s predictions from Wall Street proved again that the consensus is rarely correct.

The current view of the economy is that large interest rate hikes of the past year will finally be felt, causing growth to slow. How much is where the divergence in opinion occurs. The range is wide, but most call for the U.S. to have a soft landing or mild recession followed by a recovery. Fiscal policies in 2023 offset Fed tightening. Now the Fed will begin to lower rates beginning in March, or soon thereafter, as the economy slows. This gives ballast to both long dated bonds and stocks if the recission is mild.

Most predictions for the S&P 500 call for modest gains. In total, the range of predictions is comically wide. BCA Research is the most bearish, projecting a recession that drops the S&P 500 26% from current levels to 3,500. Dr. Ed Yardeni owns the most bullish call we’ve seen, with a 2024 year-end target of 5,400, or about 13% gain from current levels. For what it’s worth, Yardeni has been the most accurate forecaster we’ve followed since the pandemic.

Valuations are relatively expensive. According to FactSet, the S&P 500 forward P/E is presently 19.3x. The five-year average is 18.8x while the ten-year average is 17.6x. Earnings remain hard to predict, with a $237 estimate in 2024 by Goldman Sachs giving us a 20.0x P/E and a 5% earnings yield with the index at 4,735. This compares to 4% on the 10-year government note.

We remain confident in the U.S. economy’s strength across both short and long-term horizons. Our technology leadership creates economic leadership. Relative to other large economies, America offers a compelling package of stable governance, rule of law, reasonable regulations, and a culture of innovation. These factors and the dollar’s reserve currency status solidifies the U.S. as the premier economy for investment.

Thank you for your continued trust and partnership. We will stay curious, embrace change, and capitalize on the opportunities that lie ahead.