May 6, 2025

April Market Recap: Policy-Driven Volatility

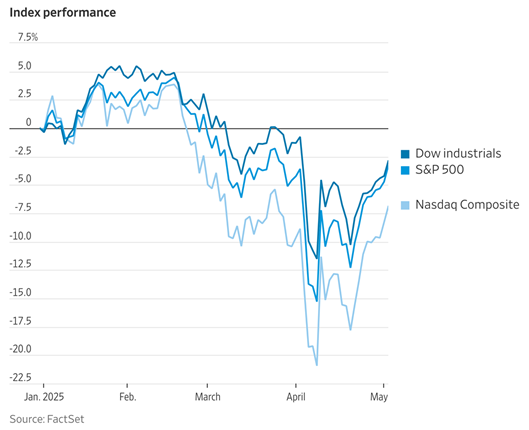

April was a turbulent month for markets, sparked by President Trump’s sweeping tariff announcement on April 2nd. The S&P 500 plunged nearly 10% over the next two days, its worst two-day loss since March 2020 — wiping out over $6.6 trillion in market value. A partial tariff pause on April 9th triggered the S&P’s best single day since 2008. Stocks, bonds, Treasuries, and the dollar all sold off at several points, leading traders to label the pattern the “Anything but America” trade. The month ended with a nine-day winning streak, the longest since 2004, helping the S&P 500 and Nasdaq recover nearly all their earlier losses.

When the dust settled at the end of April, it looked as though nothing much happened. The S&P 500 lost just 0.8% and the Nasdaq managed a modest gain of 0.9%.

Market volatility was extreme, but headline numbers didn’t reflect the drama beneath the surface. Leadership shifted quickly throughout the month, and sentiment remains fragile.

The tariff announcement marked a major shift in U.S. trade policy. President Trump introduced broad-based import taxes: 10% across the board, 34% on Chinese goods, 25% on cars, and 20% on EU goods. China quickly retaliated with its own tariffs, and the EU followed suit. A 90-day pause in some tariffs helped stabilize markets, but China was excluded, with U.S. tariffs on Chinese goods raised even higher.

The uncertainty created by these moves makes it difficult for businesses to plan and spend. Strategists slashed S&P 500 year-end targets and increased the probability of a recession. Goldman Sachs raised its recession odds to 45%, citing trade risks and fragile sentiment.

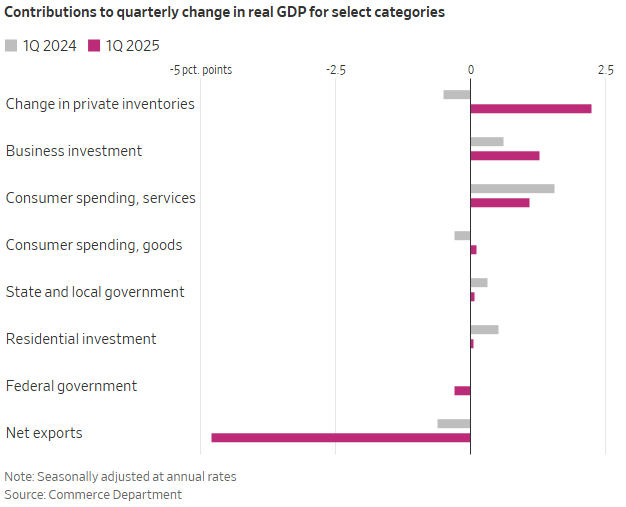

First quarter GDP fell 0.3%, contracting for the first time since early 2022. Upon further inspection, there was a good amount of strength in the report. Much of the contraction came from businesses front-loading imports before tariffs. Imports are subtracted from GDP. At a minimum, the report showed how tariffs impacted the economy even prior to being implemented. Q2 will be highly scrutinized.

The labor market cooled, with private hiring slowing sharply in April. Still, the April jobs report released May 2nd beat expectations, showing economic resilience.

Bond markets failed to act as a safe haven. As equities sold off, Treasuries also came under pressure. The 10-year yield moved wildly during the month, falling below 4%, spiking above 4.5%, and settling around 4.2%. Typically, when stocks fall, bonds rally. That didn’t happen in April, which injected more uncertainty into global markets.

Corporate earnings remain a bright spot. Q1 earnings season is nearly complete, and FactSet is projecting that S&P 500 year-over-year earnings growth will be over 10%. This will be the second straight quarter of double-digit gains. Revenue growth was also positive across most sectors. This strength suggests that companies are managing well for now, but many CFOs and CEOs are flagging concern about future quarters if tariffs remain in place.

Markets are forward-looking, but sometimes they overlook what’s right in front of them. Optimism at the end of April may not fully account for the policy risks that lie ahead. Prolonged negotiations or deeper supply chain disruptions could pressure earnings later this year. Small businesses and farmers, both sensitive to trade costs, are particularly vulnerable. For now, the market is betting that the White House will continue to backpedal.

Despite the uncertainty, there are signs of resilience. Gas and food prices have come down. Consumer spending remains solid in some areas. But overall sentiment has weakened, and policy remains a wildcard. The Federal Reserve meets tomorrow, but no major moves are expected. Inflation data in the days following the meeting could set the tone for rate expectations in June.

Historically, May tends to be a positive month for markets, but this year will hinge on how trade issues evolve. The market appears to be priced for quick deals and a return to stability. If that doesn’t materialize, volatility could return just as quickly as it subsided in late April.

Drawing on our Investment Committee’s experience, it seems politics have taken the wheel for now. These periods are typically short-lived, but in the moment, headlines often outweigh fundamentals. Over the coming months, we expect the noise from politics and trade to fade, allowing markets to refocus on the more durable drivers of earnings and interest rates.

As always, our approach remains focused on long-term goals. In uncertain environments, reacting to short-term news can be costly. Our job is to navigate volatility without being consumed by it. Thank you for your continued trust.