April 1, 2024

First Quarter 2024 in the Books

The S&P 500 was up 10.2% for the first three months of the year. That is only the fourth time since this millennium began that Q1 rose more than 8%. Overall, the index has managed an 8% gain or more during Q1 only 17 times since 1950.

Combined with the 24% surge last year, U.S. stocks have been “the place to be” for investors worldwide.

AAII Investor Sentiment Survey reports 50% Bulls, 27.6% Neutral, 22.4% Bears as of 3/27/2024. Investor enthusiasm tends to rise as markets rise, and now is no exception.

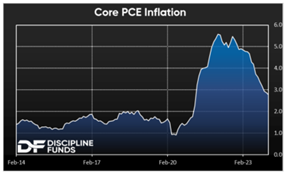

The latest core PCE inflation gauge was reported last Friday at 2.8%, the lowest in three years. This is the Fed’s preferred inflation gauge and has been on a downward trend. Atlanta Fed’s Nowcast says the March reading will come in at 2.7%, continuing the trend and giving investors more confidence that the Fed will start cutting rates in the summer.

Given the fact that the long-anticipated recession in the U.S. has yet to arrive, the Fed has not begun to lower their federal funds rates which remain above 5%.

Japan has joined Europe in finally ending negative interest rates this past month. Most of the world stock markets are rising, and even China is emerging from its long slump.

The iShares Aggregated Bond Index (Ticker: AGG) was down 1.6% year-to-date. Stocks had hefty gains, with the exception of small caps. The long-dated US Treasury 20+ Bond ETF lost 4.5% in the quarter.

The market continues to be led by growth names with iShares S&P 500 Growth ETF up 10.4% while iShares Value gained just 3.3%. NVDA soared 82.4%, META +37.1%.

The Magnificent 7 seems to have lost two stocks this year with TSLA -30.6% and Apple -10.9% in the first quarter.

The investment consensus looks for the Fed to ease soon and do so up to three more times before year end.

T Rowe Price sees S&P 500 earnings up year over year 9.5% and 13.9%, in 2024 and 2025, respectively. This backdrop in a Presidential election year is positive for a continued rally in stocks.

Our concern in the near term is that the market is now overbought and could use a breather to refresh enthusiasm. Additionally, short-term US Treasures yield 5% plus. Longer dated bonds rallying over the next nine months would ease valuation concerns.

The U.S. national debt is now $34 trillion and growing by $1 trillion every 100 days (https://usdebtclock.org/). This will present its own set of challenges to any new administration and Congress in 2025 and beyond. As investors, we don’t need to be concerned with the national debt until the bond market is concerned.

We wish you a Happy Spring!