March 4, 2025

Late February Slide Continues into March

Quick update on the recent market pullback:

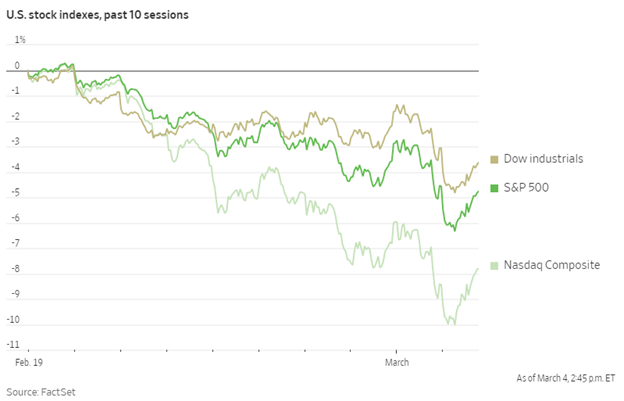

- The S&P 500 hit an all-time high just 10 trading days ago on February 19th

- Since then, the index is down about 6%

- Today, the Nasdaq traded down to a correction of -10% from its December 16th all-time high

- Soft economic data from late February and new tariffs being implemented this week are the main causes for the pullback

- Stocks have been at historically high valuations during the current bull market. When this occurs, the market is susceptible to negative catalysts which can lead to sharp pullbacks like we’ve seen in the last two weeks.

- The economy remains strong. Q4 earnings season had the highest growth rate in three years, according to FactSet.

- Ultimately, we believe this is momentum unwinding due to the possibility of slowing growth rather than the start of long downtrends in the economy and stock market.

- We expect the volatility to continue with each material announcement from the White House and Fed in the coming weeks.

Back to our regularly scheduled programming:

February lived up to its reputation as a bane to stock markets gains. The month erased Nasdaq gains for the new year to date and nearly wiped out the gains in the S&P 500.

Negative sentiment reached near record levels as Bears in the AAII sentiment survey of individual investors went above 60%. Tariff targets in Canada, China, Europe and Mexico are concerning investors.

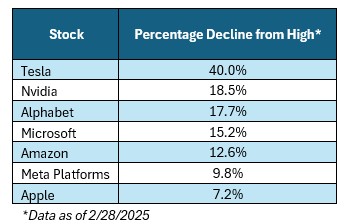

Despite their pivotal role in propelling the market’s gains last year, Magnificent Seven stocks have recently experienced significant downturns. Specifically, five have entered correction territory, marking a sharp reversal from their previous highs and damaging overall market momentum.

On the positive side, bond yields on the 10-Year US Treasury have declined to 4.2%, even though the Federal Reserve has signaled they are on hold with rate cuts for now. This drop in yields reflects growing expectations for slower economic growth and potential monetary easing later in the year.

Speaking of cuts, the DOGE (Department of Government Efficiency) is taking a knife to federal government jobs, which will likely push unemployment numbers higher in the near future. This could weigh on consumer confidence and spending in the months ahead.

Scott Bessent, our new Treasury Secretary, is laser-focused on getting interest rates low enough to facilitate the massive amount of new debt our country needs to finance its bloated budget. Managing this delicate balance between funding needs and market stability will be crucial in the coming quarters.

European markets have far outpaced the US in 2025, rising 14% through February. This strong performance is likely driven by lower valuations relative to U.S. stocks and renewed hopes for a peaceful resolution in Ukraine.

Gold continues to climb as geopolitical and economic risks around the world increase. The precious metals’ strength reflects investor demand for safe-haven assets amid global uncertainty.

The US dollar has remained steady despite ongoing geopolitical tensions. Even after a ceasefire, tensions between Israel and Gaza remain high, adding to the atmosphere of caution in global markets.

Earnings estimates for the S&P 500 were as high as +13% for 2025, but those forecasts are starting to come down as worries about the economy grow. The Atlanta Fed now projects -2.4% GDP growth for the first quarter, suggesting a slowdown that could impact corporate profits.

Budget battles loom in the House of Representatives and the Senate, with debates over spending and debt likely to add more volatility to markets.

Despite the current market pullback, the economy remains strong with Q4 earnings showing a 17.8% y/y growth, the highest since Q4 2021 according to FactSet. We expect continued volatility but see this as a healthy reset, not the start of a prolonged downturn.

Wishing you a sunny end to winter.