July 9, 2024

Summertime and the Livin’ Is Easy

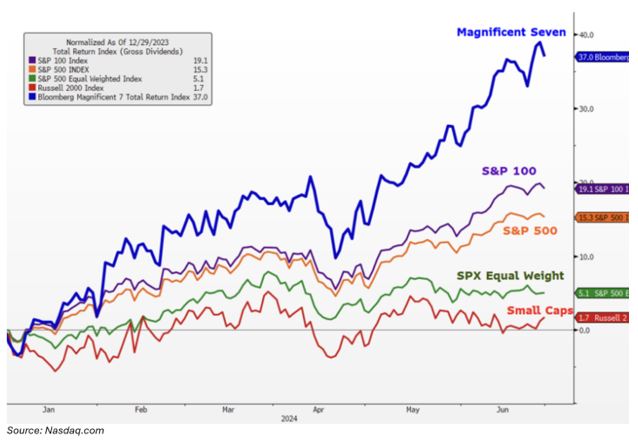

In the first half of the year, the S&P 500 surged 14.5%, marking the second-best performance since 2000, according to Bloomberg.

Out of the 500 companies in the index, the leading technology stocks, i.e. the Magnificent 7, accounted for 62% of the total gains for the index. They led the parade like last year due to their enormous earnings gains and investors’ enthusiasm in artificial intelligence (A.I.), effectively creating a bifurcated market.

The Nasdaq grew 18.1% while the Russell 2000 gained a lowly 1.0%. The Dow Jones also fared poorly at 0.9%. Gold gained 12.9%, and WTI Oil +13.8%.

The 2-year U.S. Treasury Note finished June at 4.71%, adding 48 basis points since December 31st, while 10-year U.S. Treasuries closed the month with a 4.36% yield, up from 4.06% at the start of 2024.

We have yet to get a rate cut from the Fed who keeps on hinting of one any time in the not-too-distant future. The year started with expectations of six rate cuts. The market now expects two, with the first in September.

Three-month to twelve-month U.S. Treasury Bills continue to yield excess of 5% risk-free, far surpassing the current 1.23% dividend yield on the S&P 500 index.

The forward earnings yield on the index using a $275 estimate stands at 4.9%. The difference of this yield versus the U.S. 10-year Note at 4.36% indicates little upside in stocks unless treasury yields drop significantly, or earnings broaden out and gain impressively from here.

A.I. stocks are the driving factor for both earning gains and rising P/E ratios. Nvidia surpassed both Apple and Microsoft in the $3 trillion club in late June, briefly becoming the largest capitalization in the world, exceeding in value the entire German stock market.

With the Fed now anticipated to lower rates in September, a pickup in the more leveraged small capitalization names, which are far more interest sensitive, is anticipated by many pundits.

Consumer spending has slowed, and savings rates are up-ticking of late as inflation remains subdued, but still above the 2% Federal Reserve target.

While July has gotten off to its typical strong start, greater volatility can be expected than that experienced so far in 2024. Both domestic and global events may soon create more uncertainty than the typical 4-year cycle serves up.

If the past couple of weeks is any indication, the November election is likely to create a good amount of uncertainty. Stock prices generally go down when uncertainty goes up. After elections, stocks tend to rally as the uncertainty concludes.

Our goal is to focus on fundamentals and not get caught off guard. So far, so good with our strategies.

We wish you a happy and perhaps even an adventurous summer.

Please contact us with questions should any come to mind.