Earnings Prevail Over Noise

July saw new all-time highs in both the NASDAQ and S&P 500 as positive earnings reports prevailed over tariff headwinds. For the month, the NASDAQ rose 3.7%, while the S&P 500 climbed 2.2%—remarkably, without a single trading day moving more than ±1%.

Lots of fireworks on the 4th and throughout the month got headlines as big trade deals were reached with the EU, Japan, and Vietnam, setting new tariffs ranging from 10% with the UK, 15% for Japan and the EU, and up to 39% for Switzerland. The US appears to have set those levels without much concession to our trade partners.

Being the largest consumer nation in the world has its advantages, but we are not making any new friends in the process. China and Mexico remain in tense negotiations, while Brazil and India are still at odds with the administration.

According to Yale University, the new average U.S. tariff rate will rise to 18.3%, up from a 50-year average of just 2.5%. While that’s a dramatic shift, Yale also estimates it could add $2 trillion to federal revenue over the next decade.

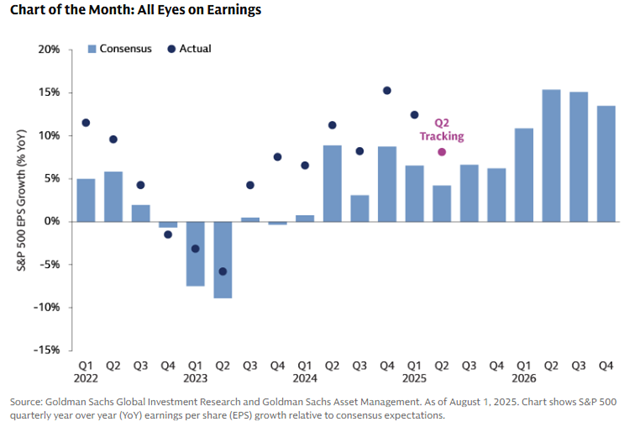

Q2 earnings season is well underway. S&P 500 earnings were expected to grow 5.8% year over year, but with two-thirds of companies having reported, actual growth stands at 10.3%, according to FactSet. Revenues have also come in strong, beating both expectations and year-ago levels.

In sum, earnings are trumping Trump policy in the stock market.

Interestingly, the most important detail of earnings seasons of the last two years isn’t the earnings at all, it’s the unprecedented capital spending on AI infrastructure. Microsoft, Amazon, and Meta are on pace to spend over $100 billion combined this year to expand their data centers and cloud capabilities. In their earnings reports, they disclosed their spending is not slowing down. As long as this investment trend continues by big tech, it provides a strong thematic tailwind for the broader market.

It seems to us that this bull market is giving new life to the old Wall Street saying, “stocks climb a wall of worry”.

Much of the pessimism from earlier this year hasn’t played out. Many expected heightened uncertainty to dampen economic growth, but so far, there’s been little sign of that. The economy has shown resilience, even in the face of political and policy turbulence.

Tariffs were also expected to weigh more heavily on consumers. While some price increases have occurred, the widespread inflationary impact many feared hasn’t taken hold—at least not yet.

The AI trade has seen dramatic swings in sentiment. Earlier this year, enthusiasm gave way to skepticism as investors questioned whether the theme was overhyped. More recently, sentiment has rebounded sharply, reminding markets just how significant AI investment is to a handful of the largest stocks in the S&P 500—companies that now make up more than 30% of the index by market cap.

We also saw interest rates defy expectations. After the passage of the tax bill, many feared that the 10-year Treasury yield would rise meaningfully. Instead, it moved lower, helping to support equity valuations even as markets hit new highs.

As August unfolds, we typically see slower markets with a downward bias through September. That said, we are keeping a close eye on a few key risks.

First, any new escalation in the tariff battle with China could rattle markets. Even if new tariffs aren't immediately imposed, the risk of breakdowns in negotiations remains high. Beyond that, we’re looking to see whether the tariffs already in place begin to show up more noticeably in inflation data this fall.

Valuations are another area of focus. With the S&P 500 trading near record levels, a 5% pullback would not be surprising and would likely be a healthy reset, not a cause for alarm.

Lastly, there are some early signs that the labor market may be cooling down. While employment remains strong overall, any meaningful slowdown in job growth or wage gains could challenge the soft-landing narrative that markets have priced in.

Looking ahead, the remainder of Q2 earnings and key economic data, including jobs, inflation, and GDP, will help shape expectations. While the Federal Reserve doesn’t meet again until mid-September, the tone of the data in August will likely influence how the Fed thinks about potential policy shifts heading into the fall.