Summer is Here and the Living is Stormy

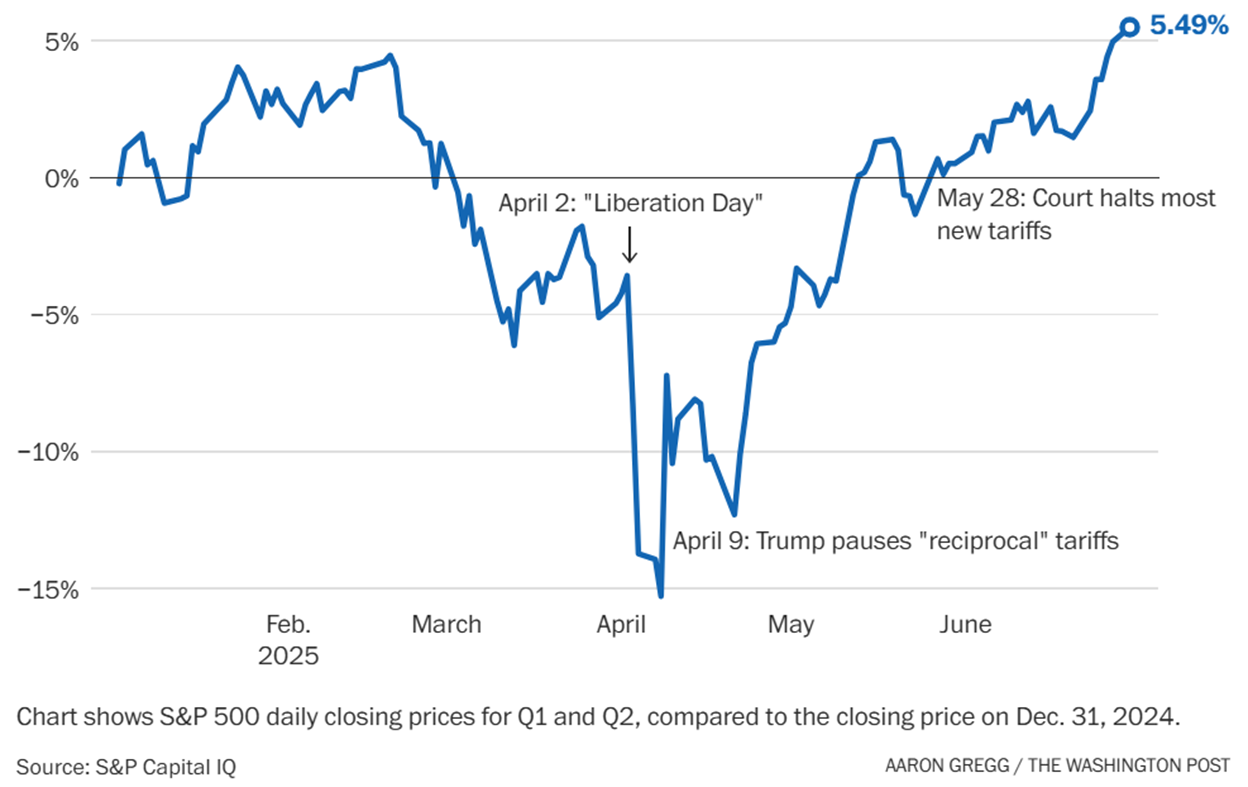

The stock market surprised many pundits with a rapid recovery from the April tariff tantrum. After a sharp 20% drop in the S&P 500 earlier this year, driven by tariff uncertainty and the administration’s “Liberation Day” announcement, stocks rebounded impressively. We closed the first half of 2025 at record highs for the S&P 500 and the Nasdaq Composite index.

Small cap indices lagged badly while foreign stock markets, developed and emerging, beat all U.S. markets, along with gold, as the US dollar sunk by 10% during this same period. The weaker dollar, marking its worst first-half decline since the 1970s, boosted foreign equities and commodities, making them attractive compared to U.S. assets.

U.S. 10-year notes saw its yield drop to 4.27% even as stocks rallied and economic policies became unclear, and war matters caught most of the headlines. Lower yields, down 31 basis points this year, reflect a market expecting calmer inflation despite global tensions.

Israel attacked Iran and the USA bombed the Iranian nuclear development sites. These events heightened fears of instability, yet markets focused on other factors, shrugging off the geopolitical noise.

One would have guessed that with all this turmoil stocks would have swooned, yet they did the opposite. Strong corporate earnings and optimism about future growth fueled a 23% rally from April’s lows, one of the fastest recoveries after a major decline.

Earnings for the S&P 500 appear to have carried the day along with lower inflation expectations. FactSet sees more growth to come as 2025 EPS expectations are 9% Y/Y while 2026 is estimated to be 13% Y/Y. Despite the lower-than-expected Q2 growth, companies delivered enough to keep investors confident.

One concern is that the earnings yield on the index is 3.4% versus 4.28% on the 10-year note. This rare gap suggests stocks are pricey compared to bonds. The 2-year US Treasury yield at 3.77% is well below the Federal funds rate at 4.31%, according to Bloomberg, signaling caution about economic growth.

The bottom line is US stocks, as represented by the S&P 500, are expensive versus historical measurements. High valuations reflect optimism but also risk if sentiment shifts. Bullish Wall Street strategists contend that elevated multiples are justified, citing the ongoing AI boom and the growing likelihood of Federal Reserve rate cuts in the near future.

As we continue to have very high and seemingly prolonged government deficit spending, given the "big beautiful bill" Congress is about to pass, stocks continue to deliver better returns than bonds both here and abroad. This spending supports market confidence, even as tariff uncertainties loom with the July 9th deadline approaching.

The fear of missing out trumps the fear of fast and furious declines. Investors, buoyed by recent gains, seem eager to stay in the market despite risks.

We have stayed patient though cautious while balancing our desire for growth with the protection of principal. Our approach ensures we pursue opportunities while safeguarding your investments in these uncertain times.

We are thankful for your loyalty and trust as we navigate these interesting times.