October 4, 2025

The Bulls are Running

The bull market rally continued to gain momentum in the third quarter. The S&P 500 and Nasdaq just posted their strongest Q3 since 2020 and their best September since 2010, according to Bloomberg. As we noted last month, September has historically been the weakest month of the year for equities, but 2025 defied that trend. The S&P 500 advanced 3.5% in September, while the Nasdaq surged 5.6%.

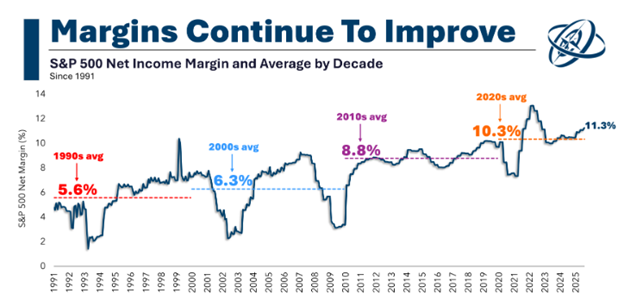

Some in the financial media have compared the current market to the dot com bubble, stoking fears of an eventual crash. We believe that comparison overlooks key differences. In the late 1990s many companies were unprofitable and traded on hopes of future growth. Today, profit margins are near record highs and earnings strength is the central driver of both stock prices and valuations. Investors are paying for real profits and proven business models rather than speculative concepts, which makes this cycle far more sustainable.

As of this writing, the S&P 500 has gone 115 trading sessions without a single day drop of 2% or more, its longest streak since July 2024. Since the April tariff scare, the index has climbed 35%, underscoring just how durable this rally has been.

We continue to see technology stocks leading the parade, but broader participation is emerging. The U.S. Total Stock Index rose 8.7%, reflecting strength beyond mega cap technology. Earnings momentum and falling interest rates are fueling this advance. The Federal Reserve lowered its policy rate by a quarter point in September, and consensus now calls for at least two more cuts in the coming months. Meanwhile, the U.S. dollar has declined about 10% from last year’s peak, giving global equities a tailwind. The Global 100 Index rose 12.6% last quarter.

As always, risks remain in the backdrop. Tariff disputes, foreign conflicts, and political gridlock continue to weigh on sentiment for many investors. Yet the market’s resilience suggests the underlying economy remains solid. GDP growth has held above 3%, supported by consumer spending that is increasingly concentrated among higher income households, which now account for half of all consumption. Inflation has rebounded above 3%, a reminder that underlying pressures continue to lurk in the economy.

Recent market strength reflects a combination of powerful tailwinds: resilient U.S. growth, strong corporate earnings, an active pace of stock buybacks, Federal Reserve rate cuts, and leadership from technology and artificial intelligence. Importantly, breadth is improving as small and mid-cap stocks have begun to participate more meaningfully in the rally, broadening the market’s foundation.

That said, bull markets rarely move in straight lines. Valuations today are stretched toward the higher end of historical ranges, and history tells us that sustained runs like this often pause when a negative catalyst emerges. Whether from excessive bullish sentiment, geopolitical shocks, or a policy misstep, markets often require an external trigger to reset. While we would not be surprised by a short-term pullback before year end, we see little evidence of a lasting trend reversal on the horizon.

As always, we remain constructive on equities and neutral on fixed income, mindful that volatility is a natural part of investing but confident that the long-term backdrop continues to support asset prices.