March 4, 2026

Iran Takes Center Stage

February was a month where headline performance masked a healthy shift in market leadership. The S&P 500 slipped 0.9% for the month but remains up 0.5% for the year. The Nasdaq fell 3.4%, leaving it down 2.5% year to date, while the Dow Jones Industrial Average managed a 0.2% gain in February and sits up 1.9% for 2026. These numbers do not tell the whole story of what is happening beneath the surface.

Market attention has shifted toward the conflict in Iran. It is a serious development with real human and geopolitical consequences, yet market reactions are often far more measured than the importance of the real-world events themselves. After the first two days of March trading, both the S&P 500 and Nasdaq are down less than 1% but with increased volatility. We expect volatility to remain elevated as investors around the world gauge the likely duration of the conflict.

The primary risk we are monitoring is the Strait of Hormuz. Roughly 20% of the world’s oil and gas flows through this narrow passage. While energy prices have strengthened, we believe the impact on the U.S. consumer remains manageable unless crude oil makes a sustained move above $100 per barrel. Our strategies are built to navigate these periods of uncertainty by focusing on the economic fundamentals that outlast the headlines.

We are also watching the second order effects of this conflict on inflation and Federal Reserve policy. Treasury yields declined in February, with the 10-year Treasury yield falling back below 4%. This suggests the bond market is growing more confident that inflation pressures are moderating, which provides a supportive backdrop for interest sensitive sectors. However, a reversal of this trend is possible if the war pushes oil higher.

The U.S. consumer is entering this period of uncertainty with significant momentum. A fiscal tailwind is arriving in the form of higher tax refunds. Many households will see checks materially larger than last year due to the retroactive tax cuts that were passed last year. As we saw during the pandemic, Americans will spend the cash instead of saving. This influx of cash, combined with a wealthy retiring generation, continues to provide a solid floor for domestic spending.

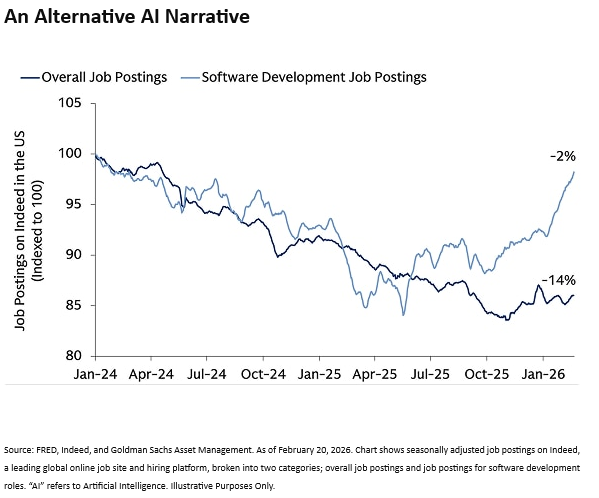

Our long-term optimistic outlook remains intact, which is rooted in a structural productivity boom. We are seeing a 2020s economy driven by technology that enhances human output rather than just replacing it. Despite fears that AI will lead to job losses, software engineer job postings are up 11% year-over-year. Software engineers were thought to be first on the AI disruption chopping block. This suggests that AI is more likely going to be an additive tool than one that replaces large swaths of skilled labor.

Finally, the corporate earnings season has been very good. This is significant. As you have read here countless times, earnings and interest rates are the two most important drivers of stock prices. Growth for the fourth quarter hit 14.2% year-over-year, easily surpassing the 8.3% estimates, according to FactSet. With double-digit profit growth projected for every quarter in 2026, the fundamental foundation of this market remains strong. We believe the current volatility is a period of normal rebalancing rather than the end of the bull market.

We are staying alert to risks like private credit and new tariffs, but the weight of economic evidence remains constructive. We appreciate the opportunity to manage your capital as we move through these changing market periods together.